Everything school didn’t teach you about compound interest

by Verve

“When is the best time to start investing?”, it’s a question we get all the time.

Our answer: as soon as you can*.

You’ve probably heard that the best way to grow your financial wealth is through investing. You may have even heard of ‘compound interest’, but if you’re not sure what it means, and why investing your money is important, don’t worry — we’re going to break it down; because, hey, we weren’t taught this stuff at school….

…well, at least not in a way that we realise ‘compounding’ can unlock incredible financial potential.

Remember, like all share based investments, your superannuation grows through the power of compound interest, so this is also a great explanation of why making even small additional contributions to your super now, can have a big impact down the track.

How does compounding interest work?

Due to the power of ‘compounding’, historically speaking, investing a dollar today is worth more than investing a dollar later. A US investment platform for women, has even estimated that every single day you wait to invest could cost you about $100 in later years, that’s like giving yourself a pay cut of nearly $3,000 a month!

It might sound crazy, so we’ll break it down…

Imagine that you are able to save a little over $80 a month to invest, at the end of the year you have saved $1000, so you decide to invest that money for the next 5 years. Each year that money earns a 7% return (of course in real life you will have some better years and some worse years, but let’s imagine, for this example, it’s a 7% return every year).

At the end of the first year, you will have made 7% of $1000. That’s a return of $70.00:

Year 0 (when you start): $1000.00

Year 1: $1000.00 + $70.00 = $1070.00

Now, if you leave all of that money invested, in year two you will start with $1070, and make 7% of $1070:

Year 2: $1070.00 + ($1070.00 x 7%) = $1144.90

In Year 2, you have made $74.90, because you are also making a 7% return on the $70 in interest you made the year before, this is what is known as ‘compound interest’. Let’s see how this would progress over the next three years:

Year 3: $1144.90 + ($1144.90 x 7%) = $1,225.04

Year 4: $1225.04 + ($1225.04 x 7%) = $1,310.79

Year 5: $1,310.79 + ($1,310.79 x 7%) = $1,402.54

Total returns after 5 years: $402.54

That’s the magic of compound interest.

And while earning $403 in interest over five years may not seem like much… imagine if you were investing an additional $1,000 each year for five years. Or think about your superannuation and the tens, if not hundreds of thousands of dollars that many of us will invest into super over 40+ years of our working lives.

Timing is key: two women, two investment outcomes

Below we’ve created an example of two fictitious women who have decided to invest. Mel has decided to save and invest $100 a month and starts at age 30, whereas Vanita doesn’t start investing until age 40, but then decides to catch up and invest $200 a month. Check out how much they invest, and how much they earn from their investments assuming both receive a constant return of 7% p.a.

The lesson: get going early, but better late than never!

The Australian Government MoneySmart website has a great compound interest calculator, you can experiment with different investment values and see how much you could earn.

Investment returns come with risk, here’s how to weigh it up

What you’re probably thinking right now is sure, but what about the global financial crisis? Um.. what happens if I invest in shares and the market drops? Well, good question!

Every investment you make comes with risk, when it comes to shares typically shares with higher potential returns also come with higher risk. Now, let’s have a look at what that means in reality by comparing two types of investments over the past few decades.

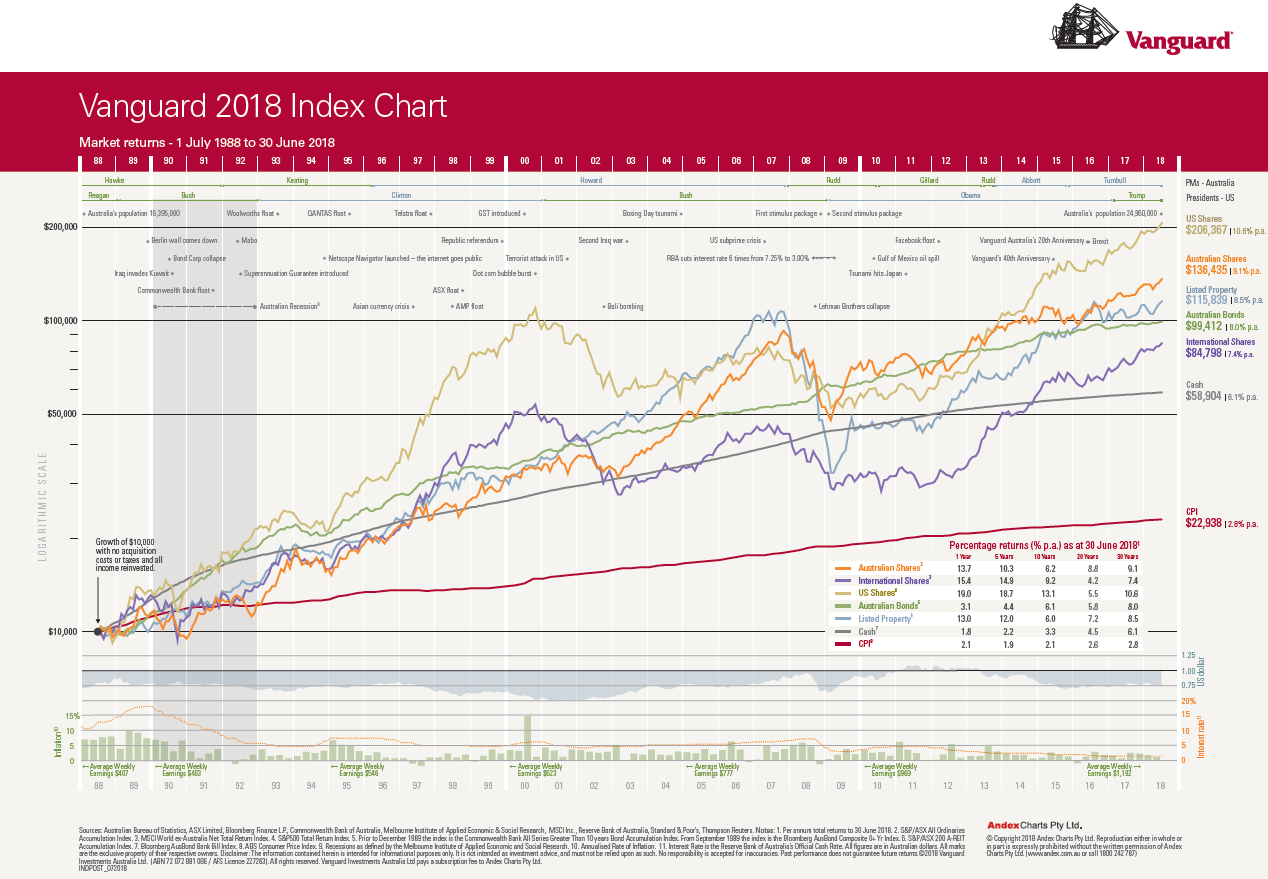

Take a look at this graph of the share market over the past 30 years, you’ll see that if you had invested in ‘cash assets’ which are typically the safest kind of asset (note: this is not the same as having cash in your bank), then you basically would have more-or-less made a profit each year and an average profit of 6.1% p.a. If you had invested $10,000, by 2018 you would have around $58,904. That’s not bad.

By contrast, if you had invested your $10,000 in the companies on the Australian Stock Exchange (ASX), you would have made money most years but you would have also lost money in some years, including suffering losses in the Global Financial Crisis in 2008/09. Yet, despite the occasional downs in the market, your gains would have been much higher and you would now have an estimated $136,435.

Stocks are typically the riskiest part of an investment portfolio, but over the past 30 year period the ASX has gone up by an average of around 9.1% p.a.

Know your goals and make a smart decision

When it comes to working out the level of risk you are willing to take, and how much you want to invest in shares, you will need to have a think about: what your saving money for; when you will want to access that money; and what would happen if you lost some of the money in the short term.

Based on the historical long-term growth of the share market, investing in shares has proven to be more useful than simply saving if you want to achieve your money goals and build financial wealth.

As a next step, check out the MoneySmart website to assess your own level of risk and what kind of investment is most likely to suit your savings goals.

If you’re a member of Verve Super, head to the Verve Academy and learn more in the investment learning module, including how to get started!

*Of course there is an asterix to this answer: before you make any decision to invest money, it’s important that you consider your own financial situation. As an example, if you have high cost debt (i.e. credit card debt), it’s generally better to pay that off than to invest – remember compound interest will work against you if you are in debt! Check out the Money Smart website or speak to a Financial Adviser if you want personal guidance to determine if you are ready to invest.

—

This blog is published by Verve Superannuation Pty Ltd (ABN 65 628 675 169, AFS Representative No. 001268903), which is a Corporate Authorised Representative of True Oak Investments Ltd (ABN 81 002 558 956, AFSL 238184), as the Sub-Promoter of Verve Super.

Verve Superannuation Pty Ltd and True Oak Investments Ltd are not licensed to provide personal financial advice. The information contained in this blog, including any financial guidance, is general in nature. You should consider seeking independent legal, financial, taxation or other advice to ensure that your financial decisions are suited to your unique circumstances.

You should read the Product Disclosure Statement, Additional Information Booklet, Insurance Guide, Target Market Determination and Financial Services Guide before making a decision to acquire, hold or continue to hold an interest in Verve Super. When considering financial returns, past performance is not indicative of future performance.

{kind=link}